Interest Rate Swaps: Weighing the Risks and Benefits for Your Credit Union

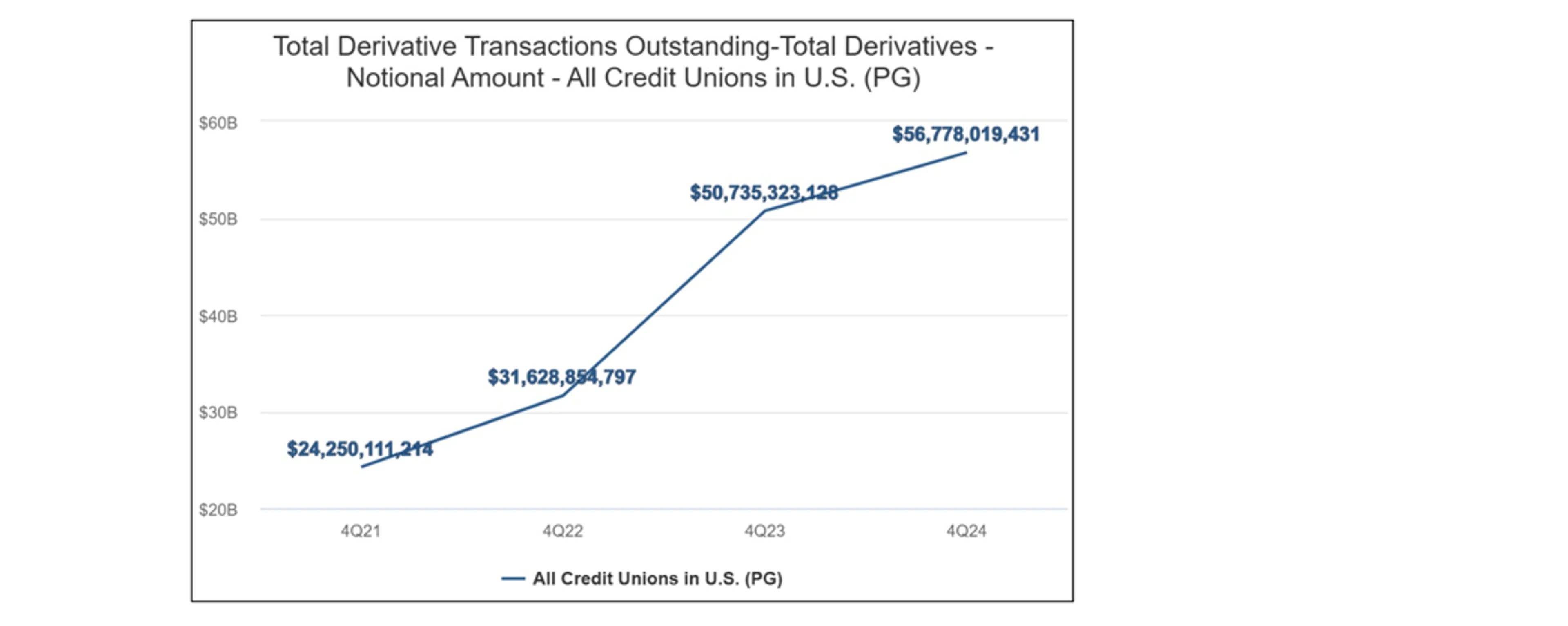

An emerging strategy implemented by credit unions to manage interest rate risk, interest rate swaps can help stabilize a financial institution’s cashflows in changing interest rate environments. The increase in derivative transactions is reflected in the graph below.

Many credit unions are using a fair value hedge strategy to directly reduce the interest rate risk associated with carrying fixed rate mortgage loans. This strategy involves entering into a pay-fixed receive-variable swap contract, which can effectively convert fixed rate interest income stream into a variable rate stream.

The increase in usage is due to both improvements in accounting and regulatory requirements, as well as the volatility in the interest rate environment. While swaps are an effective way to manage interest rate exposure, like all financial instruments, they come with pros and cons, and should be carefully considered before implementing. Doeren Mayhew’s credit union pros explore the risks and benefits that come with interest rate swaps, and the related reporting and operational requirements.

Risks and Drawbacks to Consider

- Complexity risk: Hedges put a burden on accounting and finance, and can be difficult to communicate to governance. However, as credit unions become more experienced with these transactions some of this risk will be mitigated.

- Effective Internal Controls: The National Credit Union Administration (NCUA) requires federal credit unions entering into non-mortgage banking derivatives, such as interest rate swaps, to have an internal controls review performed within the first year after commencing its first derivatives transaction. As a result, the credit union must evaluate and ensure their internal controls meet the regulatory standards well in advance and also seek out a qualified third-party provider, like Doeren Mayhew, to perform the required review.

- Counterparty risk: With most interest rate swaps being traded over the counter, it positions the credit union to assume credit exposure to the swap dealer. To mitigate this risk, you can require the swap dealer to post collateral.

- Legal documentation: When entering into a swap, there are several legal documents required in which the credit union may need to seek counsel or an advisor specializing in interest rate swaps to conduct a review.

Understanding the Benefits

- Effective risk management tool: If you’re looking for an effective tool to manage your credit union’s interest rate risk, doing an interest rate swap can help achieve this. Interest rate swaps might be considered insurance, whereby a premium is paid to stabilize net economic values in changing interest rate environments.

- Tailored to fit your needs: From timing to structure, and more, interest rate swaps can be designed to meet the specific needs of your credit union. Many credit unions create strategies to both reduce risk and increase return on assets as compared to alternative strategies.

With an ever-changing economy, interest rate swaps have continued to increase in popularity amongst credit unions. Whether you’re looking to explore derivatives or seeking out a credit union auditor to perform a review of your existing derivative program, Doeren Mayhew’s Financial Institutions Group has the knowledge and industry expertise to help strengthen your controls and pave the way for long-term success.